Economic trends facing business in 2022 and beyond

Editor’s note: This article is part of an annual four-part series on trends impacting small and midsize businesses. In Part 4, we study economic trends for 2022.

Amid unprecedented supply chain shocks, labor shortages and inflation, business owners are reconciling which economic conditions are transitory and which are permanent.

President Biden’s announcement re-nominating Federal Reserve Chair Jerome Powell for a second term was widely viewed as an endorsement of current Fed policy, which has favored full employment over arresting inflation.i The demand for goods, ongoing port congestion and shortages of everything from truck drivers to restaurant staff is constraining the U.S. economy.

Our current state is a shortage economy in chaos:

- Inflation at 6.2%, the highest in 31 years.

- Central banks fueling a COVID response through various quantitative easing techniques, pumping over $10.4 Trillion into the global economy.ii

- A total of $12 trillion in COVID-related stimulus from the U.S. government.

- Extended unemployment rates, accelerated retirements and other factors reducing the American labor participation rate to 68%.

- A sudden spike in energy prices, in part fueled by undersupply of natural gas in Europe, and a global shift toward alternative energy.

- An armada of ships off the California coast unable to dock and ship goods, causing downstream supply chain disruptions.

- De-globalization resetting the world order for trade policy based on rivalries rather than the natural laws of supply and demand.

- Surging demand for electronics (including in automobiles) putting pressure on the chip manufacturing sector.

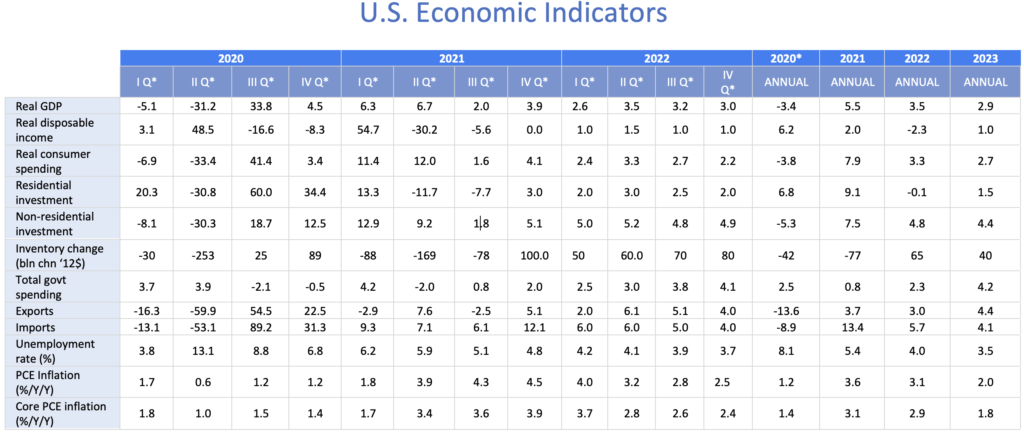

As a result of these trends, The Conference Board predicts a 5.5% increase in real GDP in 2021, slowing to 3.5% in 2022.

Other 2022 trends

Part 1: Social Trends

Part 2: Technology Trends

Part 3: Ecological Trends

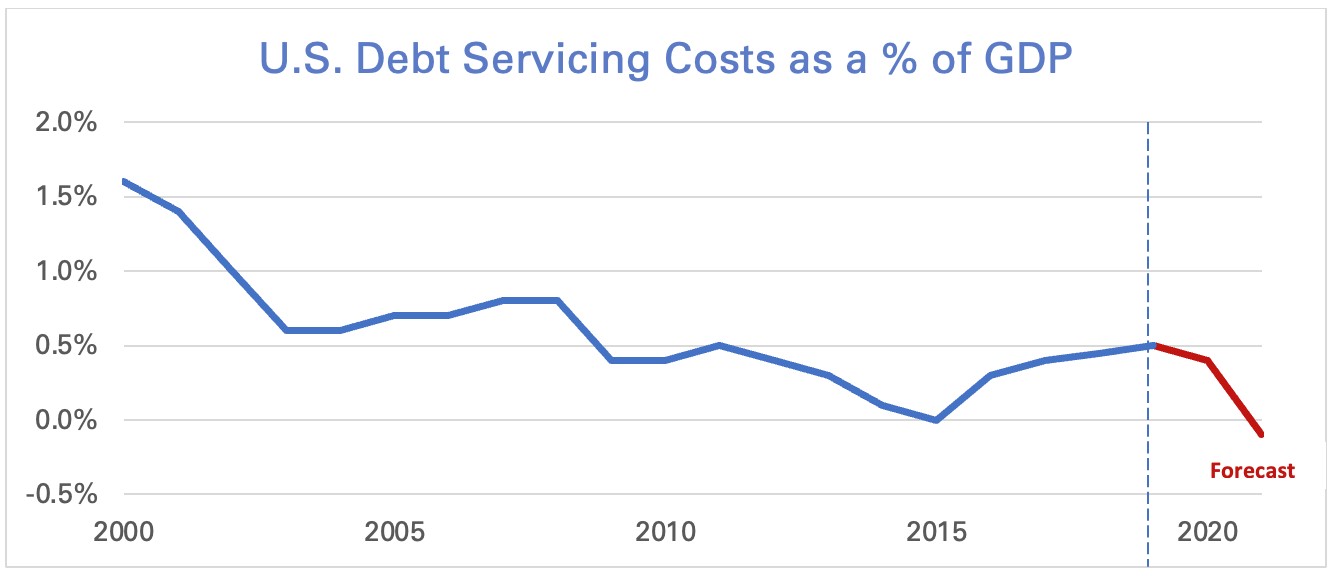

Fundamental shifts in monetary policy

After 20 years of declining interest rates, the Federal Reserve bank is posturing for multiple rate hikes over the next few quarters. At the outbreak of the pandemic, central banks had little room to drop rates as they turned negative in some parts of Europe. Instead, the Fed turned to the remaining tactic at their disposal — stimulating the flow of credit to households and businesses. These tactics have contributed to supply-and-demand imbalances. The Fed and other central banks appear resolute to keep rates low and deflate their own serving costs.

Source PIIE Charts

Long-term ramifications for the U.S. are troubling, with total federal government debt set to approach $30 trillion by the end of the year.

The infrastructure bill

On November 15, President Biden signed the $1 trillion infrastructure bill into law, allocating billions to state and local governments over the next five years. The bill is expected to contribute about a quarter of a percentage point to GDP over that time.iii The bill will fund:

- Roads, bridges and other major projects $110 billion

- Freight, passenger rail (including Amtrak) $66 billion

- Power grids $73 billion

- Improving water systems $55 billion

- Public transit $39 billion

- Electric vehicles $7.5 billion

- Electric buses and ferries $7.5 billion

- Airport and waterways $42 billion

- Climate change resilience $50 billion

- Broadband internet $65 billion

California received the most dollars ($45 billion), followed by Texas ($35 billion) and New York ($27 billion). About $650 billion is earmarked to current programs. Implementation of these projects will take years.

Not only will federal agencies have to decide which projects to fund, they must pass environmental and other regulatory reviews and then progress to local governments. The bill does codify a Trump-era mandate of “one federal decision” intended to reduce bureaucracy.iv

While as of this writing Congress had yet to pass the Build Back Better Framework, it’s clear that fiscal stimulus will not be funded by large tax increases to business owners, as Democrats had proposed.

For more detail on spending by sector, see the infrastructure bill.

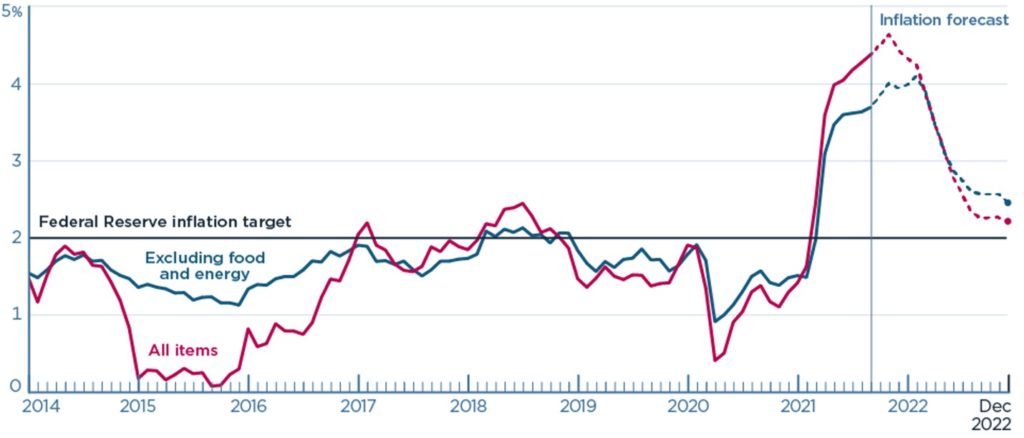

Inflation

Inflation is a function of too much money chasing too few goods and services. While it is expected that higher costs will persist through much of 2022 as markets rebalance, hyper-inflation over an extended period is unlikely. The Consumer Price Index (CPI) was up 6.2% in October, which reflects significant government stimulus and a hot U.S. labor market.

12-Month Percent Change in U.S. Consumer Prices

Source: Karen Dynan and PIIE Charts

Source: Karen Dynan and PIIE Charts

Inflation in the U.S. is outpacing the rest of the world including Europe, even amid similar COVID conditions. As supply shocks subside and higher interest rates take hold, inflation should ease by Q4 of 2022.

Visit The CEO Pulse: Inflation Resource Center

Supply chain shocks

The supply chain disruptions of the last two years represented a perfect storm. Following the longest upturn in U.S. history and a shift toward protectionism, providers leaned out their inventory and dialed back supply of key components.v The pandemic flipped a switch.

Companies are now spending 15% more to manage their supply chains than before the pandemic. Providers are gaining a better handle on the root causes of higher costs and delays. The cost of air freight from China to the U.S. was up 60% in the last three months. Canceled foreign flights that provided space for cargo have limited supply.

The Port of Los Angeles announced steep fines for operators who leave their containers in the port too long. Over 100,000 empty containers are causing a glut. Walmart began commissioning its own shipbound cargo. Underutilized passenger planes are being retrofitted for freight. Chipmakers are prioritizing their production among carmakers and electronics makers.

Retail chain executives have indicated that global supply chain shortages are receding, but that it could take a year or more for the inflow of product to normalize. The resurging pandemic is likely to cause greater disruption in supply hubs such as India and Vietnam.vi Expect volume to subside after the holidays.vii

Many raw material prices remain volatile. Many industries are reliant on a vital few sources for materials, as is the case with manufacturing buying steel and aluminum. The cost of aluminum fluctuates based on the cost of magnesium, which is controlled exclusively by Chinese providers. Total U.S. manufacturing output fell by .7% in September, even at a time of scorching demand.

The wild card in the short term may be the U.S. government. The Biden administration has announced intentions to keep tariffs (averaging 19%) on some Chinese goods in place. Companies can file for exceptions, but those will likely be hard to come by.

Two global economies

On these pages four years ago, we pondered the possibility that the tariffs would become the long-term trade policy of the United States. While the recent agreement between China and the U.S. on climate change felt like a first step, sabre rattling among the U.S., China and Russia continues.

There is an emerging bifurcation of the global economy into East and West. High transportation costs, climate change concerns and inflation are contributing to regionalization. Companies will seek to ensure supply chain continuity through vertical integration and supply chains they can control. Droves of U.S. companies are seeking just-in-time manufacturing and distribution closer to home, including in Mexico and South America.

Wages

Source: U.S. Bureau of Labor Statistics

Wages will rise 5% this year and soften slightly next year — more in the 4% range. Atlanta had the highest increase in wages in Q3 because of travel, hospitality and restaurant openings. Washington D.C. and San Jose had the lowest.viii

Food service and retail (+4.9% year over year) job wages are growing the fastest. When our economy heats or cools, low skill labor tends to migrate from one industry to another. Marketing wages are relatively flat.

Decentralized finance

A new ecosystem of financial services is emerging a result of the crypto revolution. Ethereum, a blockchain network which will work as a hub, is reaching critical mass and will reduce friction and make transactions cheap, transparent and fast. This year, Ethereum will verify $2.5 trillion in transactions—about the same as Visa.ix

The activities that take place today in banks, such as wires and loans, will happen on private networks regulated by governments. Governments with strong financial institutions like the U.S. Federal Reserve will be slower to adapt than undeveloped governments seeking out systems to stabilize their economies. Cottage industries will emerge to protect and trade assets — some in nebulous ways (such as money laundering).

Housing

Housing demand is moderating. The S&P CoreLogic Case-Shiller National Home Price Index flattened in August after rising for 14 consecutive months. Prices in 20 major U.S. cities slowed, even with lean inventory and high demand. In early November, only half of U.S. homes sold above asking price. Condos in urban areas are also rebounding. Reversing course from 2020 when multi-family landlords were offering discounts and move-in bonuses, rent is shooting up.x Residential investment represents a disproportionate level of GDP growth.

Source: The Conference Board

Source: The Conference Board

Currency risks

The U.S. dollar is performing well. The ICE US Dollar Index, which measures the dollar’s strength vs. foreign currencies, has shot up in recent months as yields on U.S. bonds shot higher. The 10-Year Treasury Bill has normalized in the 1.6% range after dropping below 1.0 through much of 2020. The U.S. is still viewed as a safe haven versus other government bonds.

Capitalists embrace carbon neutrality

As we pointed out in our post on ecological trends, there is a sea of change where business leaders are accepting responsibility to achieve carbon neutrality. Biden’s programs are certain to spark investment in electric vehicles, water resilience and other measures to combat climate change.

Car maker Rivian achieved a remarkable $130 billion in its IPO — valued higher than Ford or GM without achieving any revenue. EVs alone are expected to be a $1 trillion market by 2025.

Is retail really dead?

The death of the U.S. mall has been highly exaggerated. In 2021, retailers will open more stores than they closed for the first time since 2017.xi

While ecommerce has accelerated from 14% of retail sales in 2018 to around 20% this year, retailers are controlling distribution through brick-and-mortar and novel omnichannel experiences such as livestreaming, click-and-collect and online memberships. Walmart is partnering with TikTok, and Sephora is with Facebook.

Amazon continues to dominate many ecommerce sectors, achieving a market share of 40%.xii Others are fighting back, with Walmart alone booking $75 million in ecommerce revenue this year. Over half of retail’s gains this year will be inflation related.

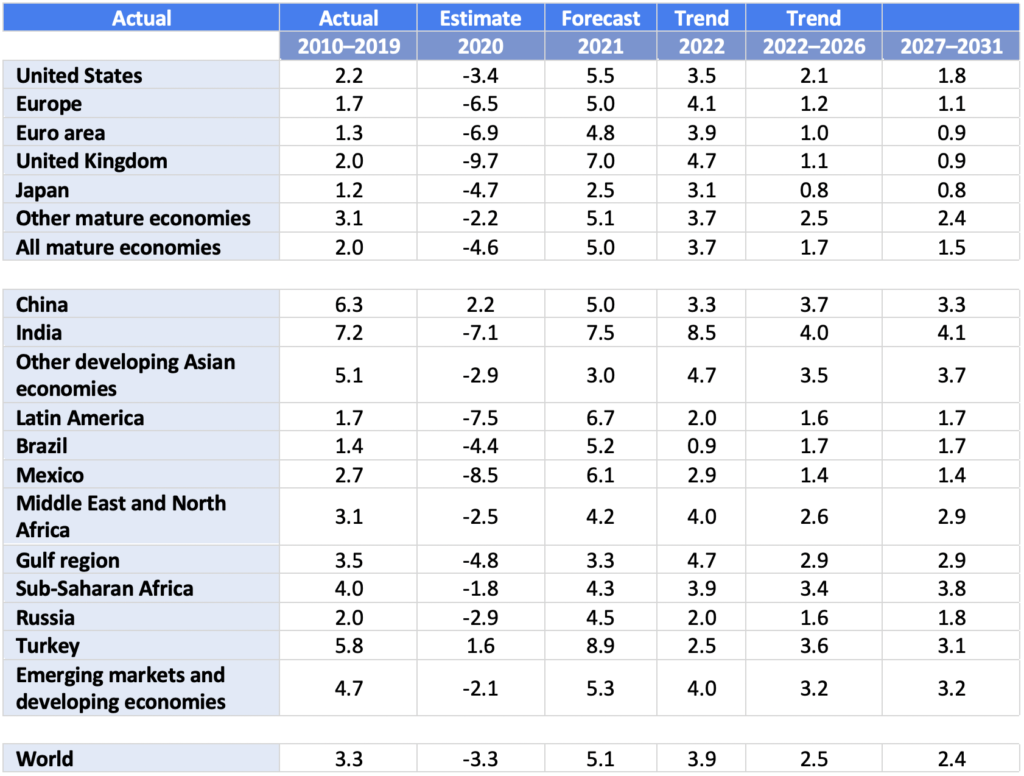

Global growth rates and risks

Given a move toward de-globalization and all that’s happening at home, we will not focus on international trends in this year’s issue. The global economy continues its recovery despite setbacks from the Delta variant, especially in undeveloped nations with low vaccination rates. Global GDP is expected to grow 5.1% in 2021, softening to 3.9% in 2022. Remarkably, China’s GDP growth has cooled to a tepid 5.0%.

Global GDP Growth Rates Source: The Conference Board

Source: The Conference Board

Trends and risks impacting global businesses include:

- COVID mutations are taking hold in Europe at a time of supply shocks and rising prices. Taking a longer view, Europe (which had a later recovery than the U.S.) will stagnate over the next five years, only growing around 1%.

- Emerging nations are more exposed to shocks in energy and food prices. A rising U.S. dollar creates a headwind for exporters. Yet some U.S. export industries such as agriculture are expected to perform well — posed to set a record in 2022 — as competing exporters like Brazil suffer from weather events.xiii

- Much of the global economy will shift toward up-leveling labor to accommodate digitization, automation and robotics.

- Among the greater threats for a global shock is a real estate meltdown in China. One of China’s largest developers, Evergrande, has momentarily averted a crisis.xiv In October the company missed a bond payment, sparking a liquidity crisis (that has since been resolved). China’s central bank continues to pump money into the system.

- Familiar geopolitical risks are still omnipresent around the world. Violence and COVID outbreaks continue in Somalia, The DRC and Nigeria. South America is unstable, with hyperinflation in Venezuela at 1,945%. Even Colombia and Ecuador, which have been stable over the last decade, have experienced unrest.

Conclusion

There has been much written about the decline of America’s standing in the world and capitalism itself. Yet statistically speaking, the U.S. economy has never been stronger in relative terms. The dollar is strong, the S&P is up 22% for the year, and hard U.S. assets appear to be the current tonic for inflation. New business starts are setting records. Our financial system is still considered the most stable in the world. Don’t take the U.S. economy for granted.

i Powell Tapped for New Fed Term by Timiraos and Restuccia, Wall Street Journal, November 23, 2021

ii The Economist, October 9, 2021

iii Biden signs $1 trillion bipartisan infrastructure bill into law, Jacob Pramuk CNBC

iv The Kiplinger Letter Vol. 98, No. 45

v The Economist, September 18, 2021

vi Global Supply Gridlock Starts to Ease by Xie, Emont and MacDonald, Wall Street Journal, November 22, 2021

vii The Kiplinger Letter Vol. 98, No. 45

viii Data Insights, Payscale

ix The Economist, September 18, 2021

x Kiplinger Letter Vol. 98, No. 46

xi Online Retailers Demand Real Store Locations by Suzanne Kapner, Wall Street Journal, November 26, 2021

xiii Kiplinger Letter Vol. 98, No. 43

xiv The Economist, September 25, 2021

Related resources

Trends facing business in 2022 and beyond

Trends facing business in 2021 and beyond

Trends impacting business in 2020 and beyond

Trends affecting business in 2019

Trends affecting your business in 2018 and beyond

Category : Economic / Future Trends

Marc Emmer is President of Optimize Inc., a management consulting firm specializing in strategic planning. Emmer is a 19-year Vistage member and a Vistage speaker. The release of his second book, “Momentum, How Companies Decide What to Do

…