Employee development tops list of how CEOs compete in talent wars [New report]

Securing the right talent is key for CEOs to realize growing revenue expectations. In fact, a recent Vistage survey shows that 71% of CEOs plan to expand their workforce in the year ahead. Unfortunately, the talent wars are impeding the ability to grow — 62% of CEOs report their ability to operate at full capacity has been impacted by hiring challenges.

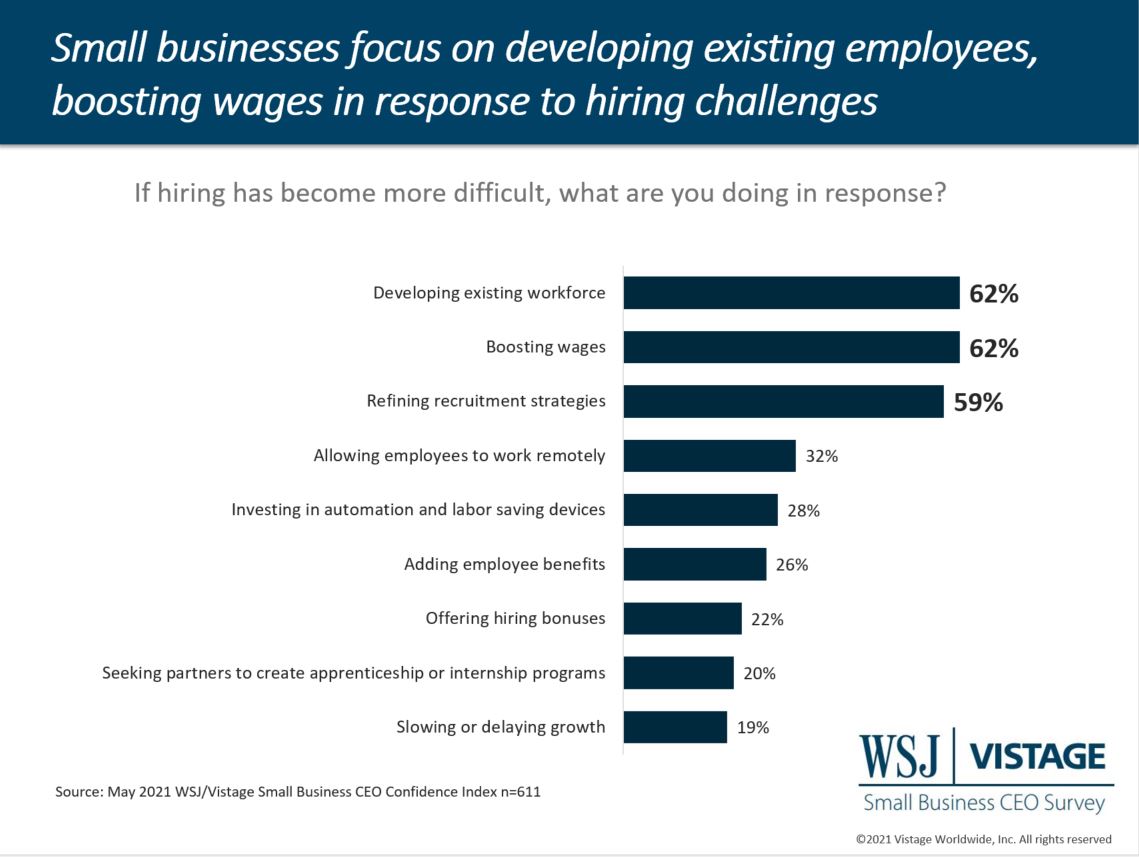

How are small and midsize businesses responding to this challenge? Overwhelmingly CEOs rely on three competitive strategies to attract and retain talent: (1) Developing the existing workforce (62%), (2) Boosting wages (62%) and (3) Refining recruitment strategies (59%).

To secure talent needed to meet demand and maximize growth, CEOs should evaluate the strength and depth of their employee development program. While employees are ultimately the beneficiary of development, these programs also offer a myriad of benefits that help businesses:

- Improve loyalty and retention

- Provide a competitive advantage in hiring

- Drive productivity and performance

Improving loyalty and retention

Competing in the talent wars starts with retaining the people you have today. Investing in employees’ personal growth improves loyalty and commitment of the existing workforce. But don’t overlook a key investment in retention — leadership development programs. Employees don’t leave bad companies, they leave bad managers. Every employee’s experience is directly influenced by their manager. Improving the leadership skills of leaders at all levels is not only an investment in their personal development, but an investment in all employees.

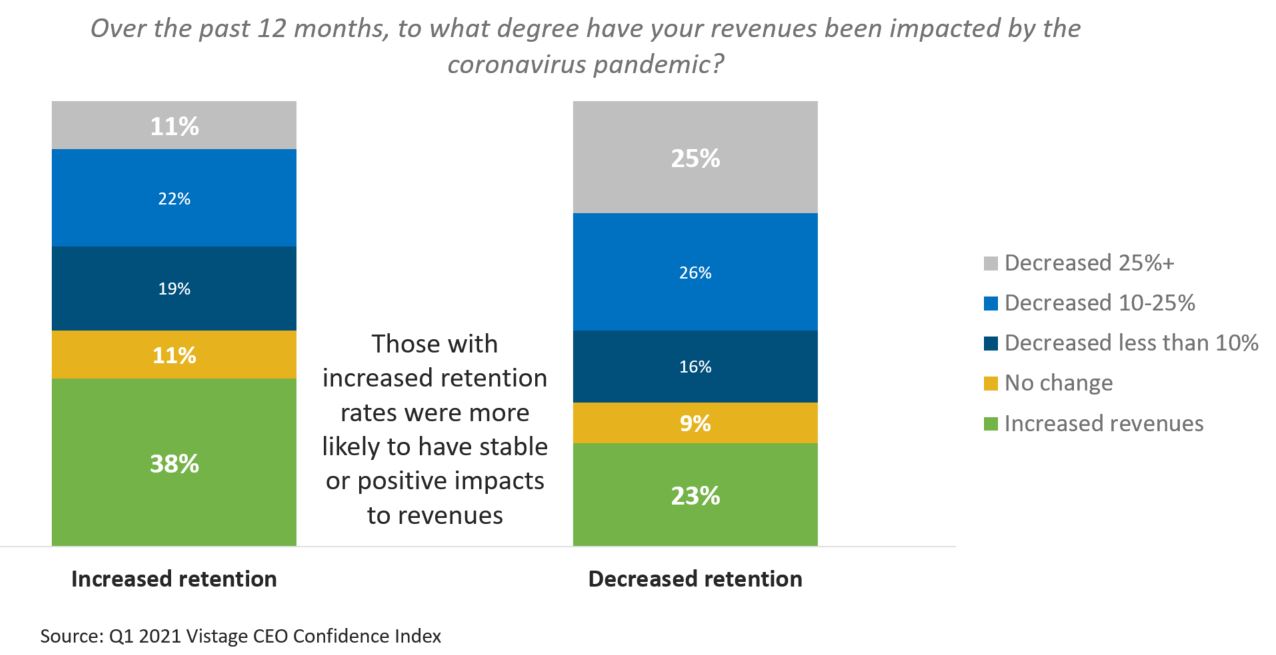

The positive impacts of retention go beyond talent metrics. Our research shows there is a direct connection between revenue and retention: CEOs who reported increased retention during the pandemic also reported stable to increased revenues at a greater rate than those who reported decreased retention. Retaining employees ensures that businesses can go beyond simply meeting demand — retention provides a solid base of talent to help them scale and take advantage of growth opportunities.

Compete to acquire top talent

Personal growth and clearly outlined career opportunities are requirements of top talent. Competitive compensation and benefits are expectations. Flexibility and remote work options are becoming new table stakes. But developmental opportunities are a key benefit that need to be outlined in recruitment campaigns and outreach.

Development programs that go beyond general onboarding and job skill requirements are key differentiators for employers. Outlining career paths and opportunities for skills and leadership development are a demonstration of a culture of growth, a culture that top talent is seeking out.

Drive productivity and performance

The capacity, capability and efficiency of employees determine a businesses’ ability to meet demand. Investing in training and development helps maintain and improve productivity in the face of hiring challenges. The ability to do more with the people they already have is a solution that helps small and midsize businesses not just maintain, but grow their business.

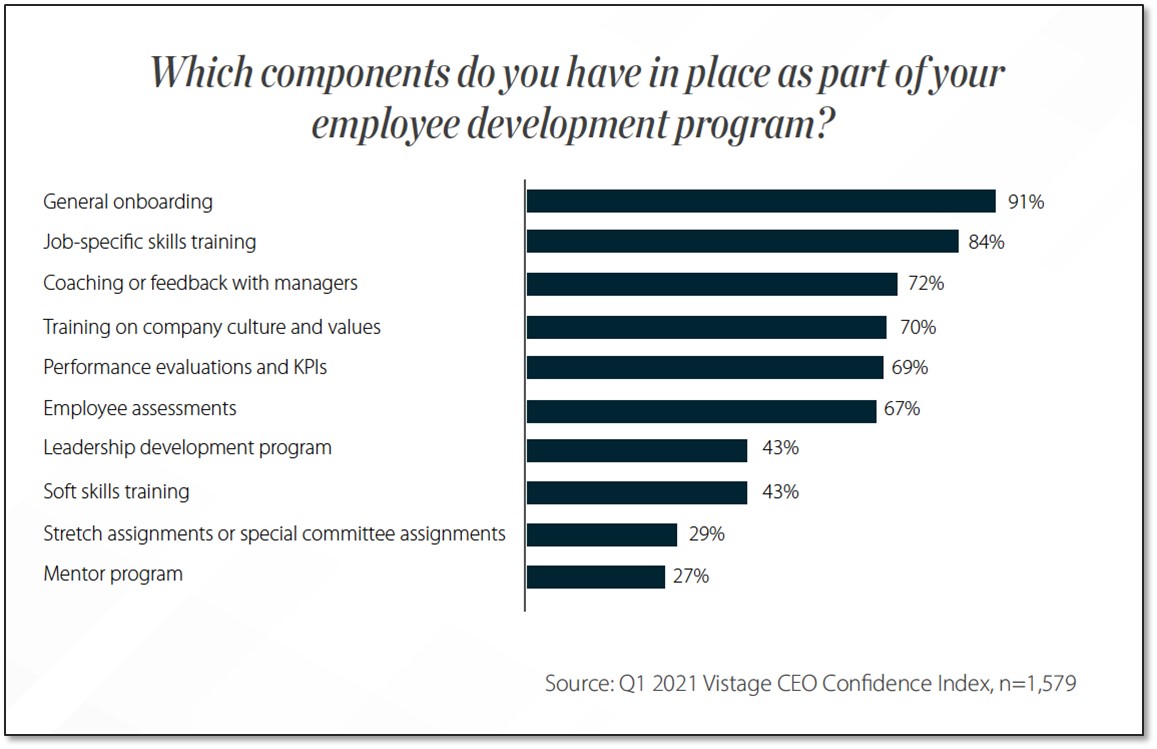

As previously stated, an increasing number of small and midsize businesses plan to expand their workforce. Growing numbers of employees also means an increasing priority to get these new hires up to speed. Our research shows that programs on the front end of the employee lifecycle are most common, with 91% of CEOs reporting they offer an onboarding program, followed by 84% who offer job skills and training. This leaves some blind spots for employees later in their tenure, something that puts employees at a retention risk.

The surge in demand is happening whether your business is ready for it or not. Many businesses have lost good people, and other top talent remains at risk in a competitive job market. Today, organizations need more than just a great strategy to succeed. They also need great employees who are both fully engaged and equipped with the right skills and competencies. Companies that commit to employee development will drive retention by demonstrating the value they place on their people and will also be effective in competing for new employees.

Category : Talent Management

As Vice President of Research for Vistage, Anne Petrik is instrumental in the creation of original thought leadership designed to inform the decision-making of CEOs of small and midsize businesses. These perspectives — shared through repo

…